Every Quote Is Free & Confidential

Every Quote Is Free & Confidential  Variable Rate MortgagesRate Usually Based On Lenders SVR |

|

Take the banking crisis of 2008 for example, the Bank of England (BoE) ultimately slashed its base rate to a record low of 0.5% and most of the lenders SVR`s were cut to reflect this. This proved hugely beneficial to some of you on variable rates, as rates were lower than they have ever been and payments reduced accordingly. Unfortunately, who knows when or if the rates will rise again? Deciding which mortgage type you are after can present somewhat of a dilemma. Fortunately for you First Choice Finance is an expert in the field and as well as searching our lender panel for the best possible deals for you, we also ask you the right questions so that you can make an informed decision.

What are Variable Rate Mortgages?

A variable rate mortgage is a mortgage or loan whereby the interest rate is periodically adjusted based on a particular index that normally reflects the cost to the lender of borrowing themselves. In many scenarios the Bank of England base rate affects this but not always directly. Generally, variable rate mortgages actually start as some kind of tracker or discounted rate mortgage and then revert; after a set period of time (ordinarily 2 to 5 years), to the lenders SVR for the rest of the mortgage term.Tracker Rate Mortgages

These mortgages are similar to and a sub type of variable rate mortgages. The difference being that this rate correlates directly with the BoE base rate or other rate that your rate is going to ``track``. Hence you may have come across the term ``base rate tracker mortgage``. This could present an advantage in that you benefit directly from a rate cut, you do not have to wait and see if the lenders SVR will follow suit and also be cut. (Although it is worth noting that the lenders normally will decide to make a similar cut, but it may not be of the same value.) Of course the BoE base rate has got very little reduction left so an upwards movement may be more likely which likewise will affect your payments due.

These mortgages are similar to and a sub type of variable rate mortgages. The difference being that this rate correlates directly with the BoE base rate or other rate that your rate is going to ``track``. Hence you may have come across the term ``base rate tracker mortgage``. This could present an advantage in that you benefit directly from a rate cut, you do not have to wait and see if the lenders SVR will follow suit and also be cut. (Although it is worth noting that the lenders normally will decide to make a similar cut, but it may not be of the same value.) Of course the BoE base rate has got very little reduction left so an upwards movement may be more likely which likewise will affect your payments due.Discount Rate Mortgages

This is where your interest rate has a discount or reduction applied to the lenders SVR for a set period of time. Again this is usually measured in whole years, typically ranging from 1 to 5. As the SVR moves up and down your discounted rate will also move up or down by the same value.If you are unsure as to which type of mortgage to opt for regarding variable rate mortgages but can see the benefits of potentially low rates right now then give us a call. We can search the market for the best deals and provide you with free quotations on multiple rates. As we provide mortgage advice we will endeavour to get you on the right type of mortgage to match your personal needs and requirements.

So who sets the Standard Variable Rate then?

We have established that variable rate mortgage`s rates are set to or linked to the lenders standard variable rate (SVR) or the Bank of England base rate. So who sets the SVR? Like any variable rate the interest rate can fluctuate and your payments can go up and down. However, unlike a tracker rate the SVR does not track above the BoE base rate at a set amount. Instead of religiously following the BoE base rate the rate you pay will be determined by your mortgage lender. It is within your mortgage lender`s jurisdiction to emulate the main market rate change or if the lender sees fit they can take a different path altogether and remain the same or even act in an opposing manner. Generally convention suggests that the SVR will move in the same direction of a BoE base rate change but not necessarily by the same amount.Potential Great Savings to be Made

Variable rate mortgages can prove beneficial in the right circumstances. Some advantages include- As it is the lenders normal rate they are less likely to have large early repayment charges.

- Arrangement fees tend to be lower than with a tracker or a fixed rate mortgage.

- They can provide necessary flexibility if you need to switch to different rates if your situation changes.

- Freedom to change mortgage provider provided any exit fees are low.

- Depending on the current economic situation rates can be very low giving you the option to over pay and bring your mortgage balance down sooner if the mortgage company allows you to.

Variable Rate Mortgages and Budgeting

When taking out any finance secured against your property you must seriously think about whether it is the right option for you. Variable rate mortgages are no different and below are some things to consider.Some potential disadvantages.

- Lenders do not always pass on the rate cuts if the BoE base rate changes.

- No rate security, the mortgage lender decides what rate you will pay.

- If you are on a tight budget you could be in a vulnerable position.

- Cannot provide certainty for your monthly outgoings.

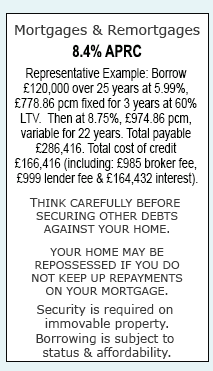

Mortgages & Remortgages |

Late repayment can cause you serious money problems. For help, go to moneyhelper.org.uk

Established In 1988. Company Registration Number 2316399. Authorised & Regulated By The Financial Conduct Authority (FCA). Firm Reference Number 302981. Mortgages & Homeowner Secured Loans Are Secured On Your Home. We Advice Upon & Arrange Mortgages & Loans. We Are Not A Lender.

First Choice Finance is a trading style of First Choice Funding Limited of 54, Wybersley Road, High Lane, Stockport, SK6 8HB. Copyright protected.